US stocks rally as a US-Iran deal nears - Newsquawk Asia-Pac Market Open

- US stocks rallied as reports throughout the session suggested the US and Iran are moving closer towards a deal to end the war. President Trump said talks have gone well and suggested he wants a deal completed before travelling to China next week, although he later added there is “never a deadline”. Sectors were broadly firmer outside of Energy and Utilities. Technology rallied, buoyed by gains in semiconductors after AMD rallied post-earnings.

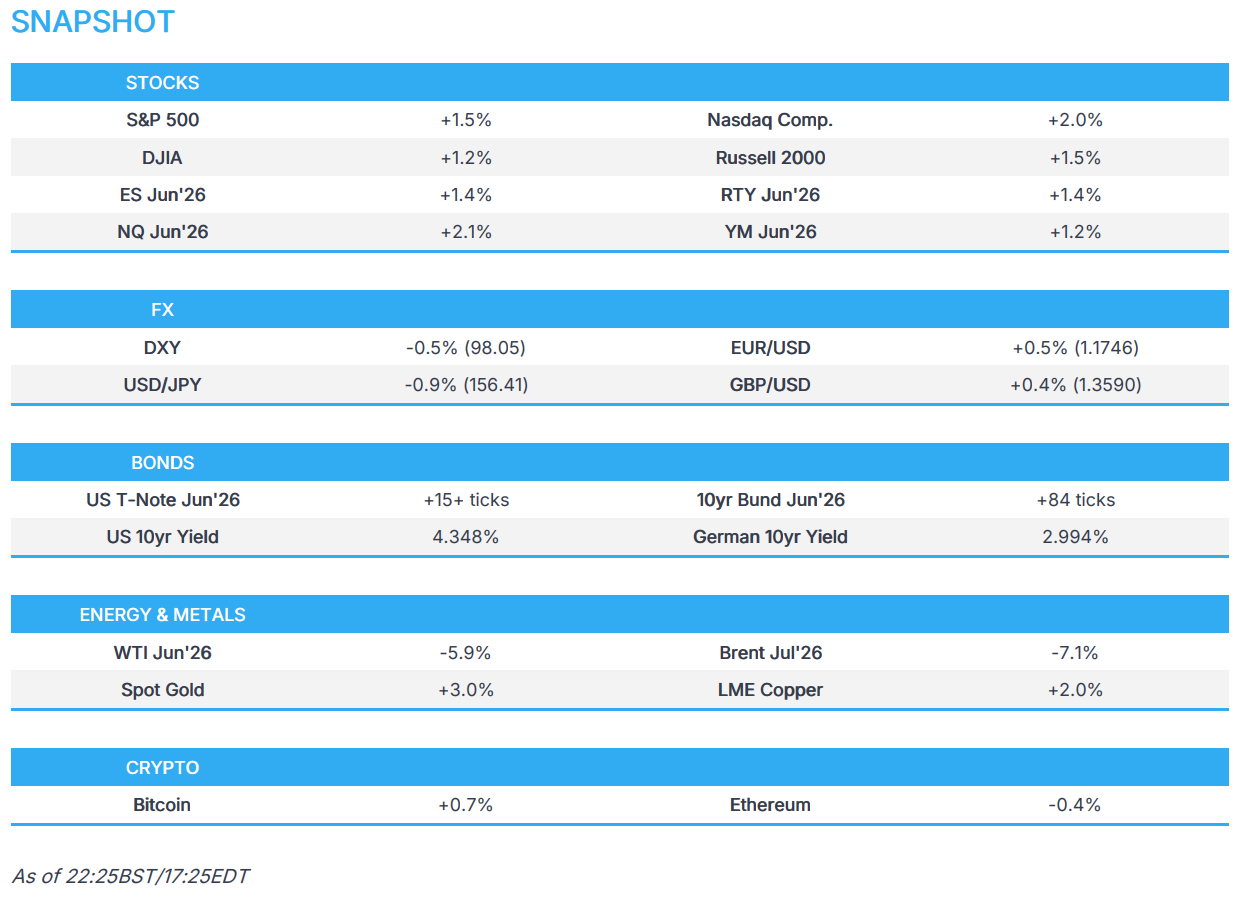

- SPX +1.46% at 7,365, NDX +2.08% at 28.599, DJI +1.24% at 49,911, RUT +1.47% at 2,887.

- Looking ahead, highlights include Australian Trade Balance (Mar), BoJ Minutes (Mar), Comments by US President Trump.

More Newsquawk in 2 steps:

1. Subscribe to the free premarket movers reports

2. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US and Iran are reportedly closing in on a one-page memo to end the war, according to Axios citing officials. The White House believes it is close to an agreement to end the war and establish a framework for detailed nuclear negotiations. The memo would be a 14-point MoU, in which many terms would depend on a final agreement being reached. On the Strait, the deal would include both sides lifting restrictions around transit through the Strait of Hormuz. On enrichment, IIran would commit to a moratorium on uranium enrichment, while also committing to never seek a nuclear weapon and would commit not to carry out weaponisation-related activities. Iran would also accept an enhanced inspections regime. The MoU would start a 30-day negotiation period, in which the US would expect Iranian responses on several key points within 48 hours.

- WSJ further reported an Iranian official stating that one idea is a halt to enrichment for 12 to 15 years before allowing Iran to enrich uranium to 3.67% purity. The official went on to add that both sides are also discussing the possible removal of some of the high-enriched stockpiles abroad, though Iran remains opposed to any such transfer to the US.

- US President Trump posted that assuming Iran agrees to give what has been agreed to, which is, perhaps a big assumption, the already Epic Fury will be at an end, and the blockade will allow the Strait to be open to all, including Iran. If they do not agree, the bombing starts, and it will be, sadly, at a much higher level and intensity than it was before. Trump later commented that the US is doing well in Iran and that Iran wants to make a deal and negotiate. He also reiterated that the US will not let Iran have a nuclear weapon and will be going to get the enriched uranium from Iran.

- US President Trump said the Iran war has a good chance of ending, according to PBS. He feels US is closing in on a deal with Iran. On a timeline, Trump said it is possible that an Iran deal can be reached before the China visit on May 14th. Fox also reported that Trump is optimistic about the Iran framework and that the timeframe is one week.

- US President Trump told The NY Post it is “too soon” to start thinking about face-to-face peace talks between the US and Iran, despite optimistic reports the two nations were closing in on a potential framework to end their 67-day war.

- US President Trump could turn to military action without an agreement with Iran ahead of the China trip, according to Axios citing US officials.

- Iran has not yet given an official response to the Americans' final text, despite claims by US media that Iran and the US are close to a final one-page agreement to end the war, according to Tasnim citing an informed source.

- Iranian Foreign Minister spokesman said Iran's response to the US has not yet been presented to Pakistan.

- Iran's advisor to Supreme Leader said Axios' text is Americans' wish list until it becomes reality, and Americans will not obtain through a failed war what they failed to gain in face-to-face negotiations. Iran has its finger on the trigger and is ready.

- What US media outlets are publishing about the details of the negotiations does not reflect the reality of what is happening, according to Al Araby citing Iranian sources.

- Iranian journalist Gholhaki, speaking on the Axios report, said "details of a potential Iran-US agreement appears to be distant from reality, at least in the nuclear domain."

- The US-Iran talks are focusing on the Strait of Hormuz at this stage, no current talks on the nuclear situation, according to Al Jazeera citing sources.

- Israel was reportedly unaware that the US was nearing a deal with Iran, and was preparing for an escalation, according to sources.

- Iranian and Saudi Arabian Foreign Ministers held a phone call, stressing the need to continue diplomacy and prevent an escalation of tensions.

- Iran has issued a message to commercial vessels in the Strait of Hormuz, saying Iran's port is fully prepared to provide general maritime services and support to the vessels, according to IRNA.

- IRGC said it will ensure the safe passage of vessels through the Strait of Hormuz.

- CMA CGM Saigon Container ship is sailing along the Omani coast after exiting the Strait of Hormuz, according to Vessel Tracking.

- CMA CGM confirmed a vessel was the target of an attack on Tuesday while it was crossing the Strait of Hormuz.

- US CENTCOM said US forces operating in the Gulf of Oman enforced blockade measures by disabling an Iranian-flagged unladen oil tanker attempting to sail toward an Iranian port at 9AM EDT on May 6th.

US TRADE

- US stocks rallied as reports throughout the session suggested the US and Iran are moving closer towards a deal to end the war. President Trump said talks have gone well and suggested he wants a deal completed before travelling to China next week, although he later added there is “never a deadline”. Sectors were broadly firmer outside of Energy and Utilities. Technology rallied, buoyed by gains in semiconductors after AMD rallied post-earnings.

- SPX +1.46% at 7,365, NDX +2.08% at 28.599, DJI +1.24% at 49,911, RUT +1.47% at 2,887.

- Click here for a detailed summary.

TARIFFS/TRADE

- USTR's Greer said the EU has had a lot of time to comply with tariff commitments, and that EU tariff and non-tariff commitments have not materialised yet. On China, Greer said the US is looking for stability with China and does not expect any decoupling from China.

CENTRAL BANKS

- Fed's Goolsbee (2027 voter) said the impact of rising productivity on inflation remains an active topic of debate. If households expect future income and wealth gains from higher productivity, it could boost spending and inflation. He added that if people pull forward future expected earnings for spending today, it could easily overheat the economy. He later stated that he is open to new ways of thinking about inflation.

- Fed's Musalem (2028 voter, hawk) said tailwinds include accommodative financial conditions are currently larger than the headwinds for the US economy, and that uncertainty around tariffs and war are headwinds. He added that there are risks to both mandates but risks have shifted towards inflation.

- NEC Director Hassett said the situation with Fed Chair Powell is still uncertain and that we are not threatening the independence of the Fed.

- BoC Governor Macklem said if oil prices keep rising and stay elevated "there may be a need for consecutive increases in the policy rate." On the other hand, if the US imposes significant new trade restrictions on Canada, a cut to policy may be needed to support economic growth. Inflation forecasts in the July monetary policy report will not change much after including the government fiscal update.

- ECB's Cipollone said the Eurozone inflation trend is moving towards adverse.

- ECB Wage Tracker: 2026 annual 2.282% (prev. 2.270%). Q1 1.847% (prev. 1.887%), Q2 2.131% (prev. 2.10%), Q3 2.553% (prev. 2.521%), Q4 2.597% (prev. 2.574%).

- The NBP kept rates unchanged at 3.75%, as expected.

DATA RECAP

- US ADP Employment Change (Apr) 109K vs. Exp. 79K (Prev. 62K, Low. 40K, High. 170K).

FX

- DXY plunged following improved US-Iran dialogue. Overnight, downside was initially spurred after President Trump announced the halt of Project Freedom, however caveated that the blockade will remain in place. However, the majority of the weakness came amid an Axios report stating that the US and Iran are reportedly closing in on a one-page memo to end the war, and the White House believes it is close to an agreement to end the war and establish a framework for detailed nuclear negotiations. However, Iran seemed to have pushed back, with Al Araby, citing Iranian sources, reporting that what US media outlets are publishing about the details of the negotiations does not reflect the reality of what is happening. DXY rebounded slightly and closed in the middle of its 97.63-98.34 range.

- EUR benefited from the dollar weakness and topped just shy of the 1.1800 handle after starting Wednesday's session below 1.1700. EZ final PMIs printed broadly in-line with its prelim. figures, in which EUR/USD failed to react.

- GBP, similarly, was driven by the softer greenback amid the geopolitical updates. Cable traded in a broad 1.3531-1.3643 range, and closed back below the 1.3600 handle. UK final PMIs did print slightly better than its prelim. figures, and resulted in a modest 10-pip move higher.

- JPY steadied around the 156.00 after the plunge earlier in the session, which seemingly came without a clear catalyst. However, with Wednesday being the last day of Japanese holidays, the move may have been as a result of MoF intervention. USD/JPY slipped from 157.79 to a trough of 155.03 before oscillating in a 155.61-156.56 range for the remainder of the session. Additionally, US Treasury Secretary Bessent is to travel to Japan next week to speak to PM Takaichi, FinMin Katayama and BoJ Gov Ueda about the weak yen.

FIXED INCOME

- T-notes rallied across the curve, led by the front-end as reports hint at progress towards the end of the war. Optimism was echoed across the US and Pakistani media, although the Iranian press attempted to downplay the progress. Nonetheless, reports suggest the two sides are discussing a 14-point framework, although negotiations still appear ongoing. Elsewhere, the Quarterly Refunding Announcement was largely in line with expectations, although the TBAC minutes hinted at a potential guidance adjustment as soon as the next refunding cycle.

- Quarterly Refunding: Announces USD 125bln refunding through July 2026 (prev. USD 125bln in Q1), to raise new cash of USD 41.7bln (prev. USD 34.8bln in Q1). Nominal coupon and FRN financing, its guidance and TIPS were maintained.

- Germany sells EUR 2.662bln vs exp. EUR 3.5bln 2.50% 2032 Bund Auction: b/c 2.4x (prev. 1.1x), avg. yield 2.8% (prev. 2.78%), retention 23.94%.

COMMODITIES

- Oil prices saw significant losses on Wednesday, given the seemingly improved US/Iran dialogue. In the European morning, which catalysed oil plummeting, Axios reported, citing officials, that the US and Iran are reportedly closing in on a one-page memo to end the war, and the White House believes it is close to an agreement to end the war and establish a framework for detailed nuclear negotiations. However, Iran continually poured cold water on the closeness of a deal, which saw benchmarks come off extremes, but still significantly lower on the session. Elsewhere, and for the record, crude and distillates saw shallower draws than anticipated in the weekly EIA data, with gasoline a larger-than-expected draw. Highlighting the breadth of energy moves, WTI traded between USD 88.66-102.70/bbl and Brent USD 96.75-109.02/bbl.

- US EIA Crude Oil Stocks Change (May/01) -2.314M exp. -2.8M (prev. -6.233M).

- Japan is reportedly to purchase 20mln barrels of UAE oil to bypass the blockade in the Strait of Hormuz, according to the Nikkei.

- India's Reliance is to shut a crude unit and other components at the 660k BPD Jamnagar refinery for maintenance.

GEOPOLITICAL

RUSSIA-UKRAINE

- Russian Foreign Ministry warned diplomatic missions and representations in Kyiv to evacuate staff in good time in the event of a mass Russian strike on the city.

EU/UK

DATA RECAP

- UK S&P Global Services PMI Final (Apr) 52.7 vs. Exp. 52 (Prev. 50.5).

- UK S&P Global Composite PMI Final (Apr) 52.6 vs. Exp. 52.0 (Prev. 50.3).

- EU S&P Global Composite PMI Final (Apr) 48.8 vs. Exp. 48.6 (Prev. 50.7).

- EU S&P Global Services PMI Final (Apr) 47.6 vs. Exp. 47.4 (Prev. 50.2).

- German S&P Global Composite PMI Final (Apr) 48.4 vs. Exp. 48.3 (Prev. 51.9).

- German S&P Global Services PMI Final (Apr) 46.9 vs. Exp. 46.9 (Prev. 50.9).

- French S&P Global Composite PMI Final (Apr) 47.6 vs. Exp. 47.6 (Prev. 48.8).

- French S&P Global Services PMI Final (Apr) 46.5 vs. Exp. 46.5 (Prev. 48.8).

- Italian S&P Global Composite PMI (Apr) 50.5 (Prev. 49.2).

- Italian S&P Global Services PMI (Apr) 49.8 vs. Exp. 48.1 (Prev. 48.8).

- Spanish S&P Global Composite PMI (Apr) 48.7 (Prev. 52.4).

- Spanish S&P Global Services PMI (Apr) 47.9 vs. Exp. 52.1 (Prev. 53.3).

- Swedish CPIF YoY Prel (Apr) Y/Y 0.8% vs exp. 1.2% (Prev. 1.6%).

- Swedish CPIF MoM Prel (Apr) M/M -0.6% vs exp. -0.2% (Prev. -0.6%).

Loading...