Futures Slump, Erasing Most Post-Fed Gains

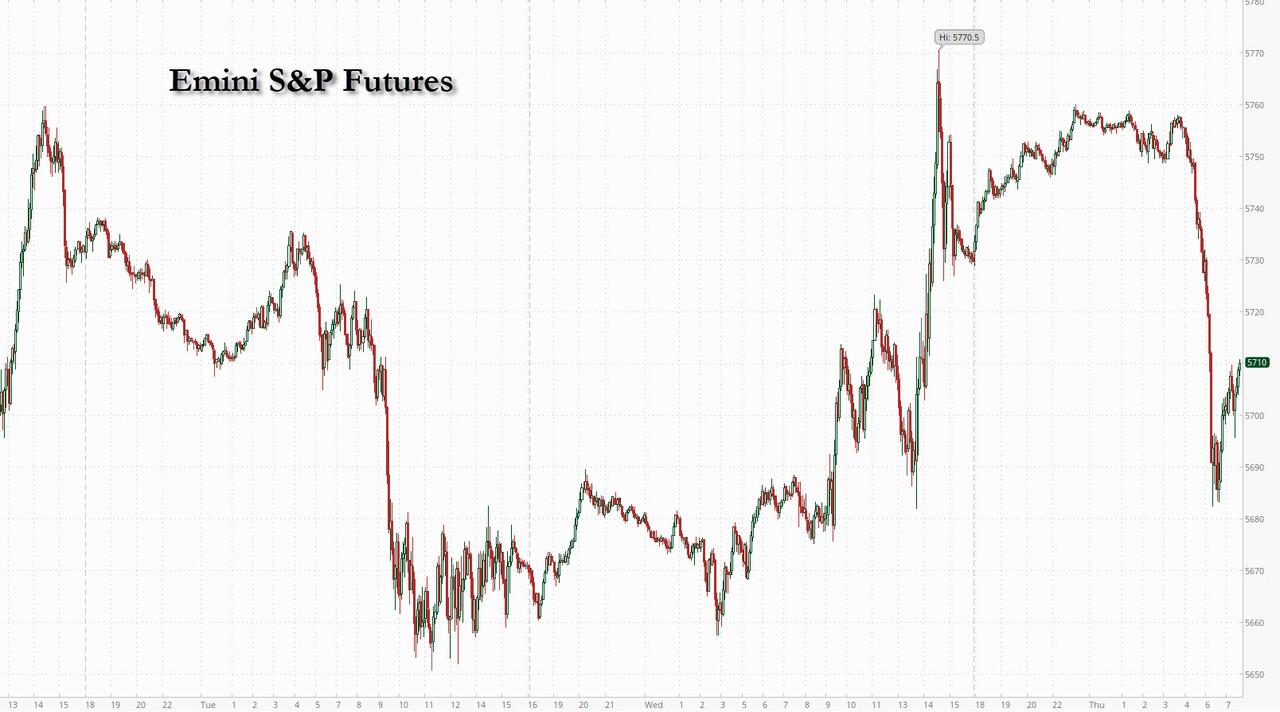

US equity futures swooned shortly after 5am ET, erasing all post-FOMC gains, as doubts grew that the Fed can significantly cut interest rates in the face of potentially inflationary trade tariffs and sentiment was weighed down by comments from ECB President Lagarde, who said that US tariffs could hit growth in the region, and couldn’t make firm commitments on interest rates. As of 8:00am S&P futures dropped 0.4% a day after Wall Street rallied on the Fed’s signal that it still sees room to ease policy this year; Nasdaq futures lost 0.6%, paring much of the earlier advance seen after Fed Chair Powell offered reassuring comments about the outlook for US growth and inflation. European stocks also dropped with the Stoxx 600 down 0.9% and are set to snap a four-day winning streak. JPM warned earlier that yesterday's rally may not be indicative of near-term direction as the Fed’s forecast shifted to support the Stagflation narrative and Powell reintroduced transitory inflation, neither are likely to give confidence to investors. Mag7 names are all loower with TSLA leading losses, while Energy and Financials are higher but Chinese ADRs under pressure. The yield curve is bull flattening after steepening yesterday; the market is still placing its heaviest bets on June and/or Sept rate cuts. USD is poised to have its strongest day in 3 weeks, which is weighing on Emerging markets. Commodities are weaker ex-WTI and Softs; gold dips below its all time high of $3,050. Today’s macro data focus is on Jobless Claims, Regional Fed activity indicators, and Housing data.

In premarket trading, Tesla slipped the most among the Magnificent Seven stocks after the electric-vehicle maker recalled all the Cybertrucks it produced and sold in the first 15 months it was on the market in the US (Alphabet -0.4%, Amazon -0.2%, Apple -0.2%, Microsoft -0.3%, Meta -0.09%, Nvidia -0.4% and Tesla -1.1%). Microchip Technology was undermined by its plan to sell depositary shares to repay debt., while US-listed shares in PDD Holdings Inc. slid as the Chinese budget-shopping site’s sales missed estimates for a third straight quarter. Here are the most notable US premarket movers:

- Akebia Therapeutics (AKBA) slumps 28% after the drugmaker launched a secondary offering of shares, with the size to be determined, via Leerink Partners and Piper Sandler.

- Aramark (ARMK) falls 2% after peer Sodexo lowered its revenue guidance, citing slower growth at its US university business.

- Cava Group (CAVA) gains 3% after an upgrade to overweight at JPMorgan.

- Celldex Therapeutics (CLDX) rises 2% after Morgan Stanley initiated coverage of the drug developer with an overweight rating, citing the firm’s compelling approach to treating a number of inflammatory conditions.

- Coty (COTY) gains 3% after Citi raised the cosmetics company to buy, saying the weakness in its consumer-beauty segment and normalization in prestige are largely reflected in the stock.

- Five Below (FIVE) jumps 9% after the discount retailer reported fourth-quarter results that beat expectations.

- PDD (PDD) ADRs fall 6% after the Chinese budget-shopping site reported sales that missed estimates for a third consecutive quarter, showing a further slowdown in growth amid pressures from domestic rivals and trade uncertainties in global markets.

- ProAssurance (PRA) surges 49% after the specialty insurer agreed to be bought by the Doctors Co., the largest US physician-owned medical malpractice insurer.

- Microchip Technology (MCHP) falls 6% after the company offered $1.35 billion in depositary shares. The group will use part of the proceeds to repay debt.

- Rivian (RIVN) slips 2% as Piper downgrades the stock to neutral, with analysts saying automakers, except for Tesla, should be avoided.

- QXO (QXO) rises 3% after the building products distributor struck a deal to buy Beacon Roofing Supply.

US markets have just endured a bruising four-week stretch in which the S&P 500 slid into a correction, but relief from assurances offered by Powell after the Fed meeting is already dissipating. Powell downplayed the economic impact of President Donald Trump’s tariff policies and said any resulting inflation bump could be transitory. The central bank also dialed back its growth forecasts for this year, while investors remain concerned about Trump’s plans to unleash a fresh tariff wave on April 2.

“The fact that the Fed Chair didn’t play to recessionary fear helped sentiment, but I am a bit bothered by his characterization of the impact of tariffs on inflation as one-off,” Wei Li, global chief investment strategist at BlackRock said on Bloomberg TV. Traders pricing as many as three Fed cuts this year could end up disappointed, Li said, adding that “markets are still expecting the Fed to be able to come to the rescue of the economy if the economy slows down, but the growth-inflation trade-off is becoming very tough indeed.”

Meanwhile, bond investors seized on the Fed’s lower growth forecasts, as well as rate-setters’ indications for a half percentage point of policy easing this year. ECB President Christine Lagarde added to the worries about the economic outlook, saying Thursday that the brewing trade war could hit growth.

European equities slipped, halting a four-day winning streak, on concern that tariffs could undercut the region’s economies. The Stoxx Europe 600 Index was down 1% by 10:40 a.m. in London, with investors taking profits on top-performing sectors including defense, banks and industrials. Sentiment was weighed down by comments from European Central Bank President Christine Lagarde, who said that US tariffs could hit growth in the region, and couldn’t make firm commitments on interest rates. Meanwhile the Swiss National Bank cut its interest rate to deter investors from pushing money into the franc. Meanwhile the Swiss National Bank cut its interest rate to deter investors from pushing money into the franc. Here are the biggest movers Thursday:

- Shaftesbury Capital gains as much as 18%, the most since 2020, after the company announced it has partnered with Norges Bank Investment Management in a deal that values the Covent Garden estate at £2.7 billion

- Eurofins shares advance as much as 6.2%, the most since June 25, after the laboratory-testing company started a new buyback program

- CVC Capital shares rise as much as 4.8%, the biggest jump since Dec. 12, after full-year earnings beat expectations, though analysts say weaker-than-expected guidance on performance-related earnings could drive downgrades

- Nexi rose as much as 5.8% in Milan trading after Corriere della Sera daily reported that US fund TPG made an offer for about EU850m for Nexi’s Digital Banking Solutions division

- Jeronimo Martins shares rise as much as 3.2% as retailer reported 4Q Ebitda beat thanks to better performance of Portuguese and Colombian chains

- Sodexo slumps as much as 18%, the most since September 2002, after the food services company issued a profit warning due to challenges including weaker growth in North America in both health care and education

- Lanxess drops as much as 9.4%, largest decline in a month, after the German chemicals company’s 2025 adjusted Ebitda guidance missed estimates. That was mostly due to prebuying in 4Q, Citi says

- 3i Group shares fall as much as 8.3%, the steepest decline since May 2022, after the private equity firm gave an update on its biggest portfolio company that analysts said was disappointing

- Investec falls as much as 4.6% in Johannesburg, the most since December, after the bank said it expects its basic earnings per share for the full year to fall by as much as 36% compared to the prior year

- Husqvarna falls as much as 4.5% as SEB Equities lowers its price target to a new Street-low and trims 2025-27 EPS estimates by 11%-12%, citing soft sentiment in Europe and a “clearly weakening” US environment

Earlier in the session, Asian stocks were mixed as investors sold Chinese shares, offsetting optimism elsewhere after the Federal Reserve signaled there’s still room to ease policy later this year. The MSCI Asia Pacific ex-Japan Index was little changed. Shares advanced in Taiwan, South Korea and Australia, while Indonesian stocks extended a rebound for a second day. Japanese markets were shut for a holiday. A gauge of Chinese shares listed in Hong Kong posted its biggest drop in three weeks, with some market participants attributing the losses to profit taking and waning earnings catalysts. Onshore Chinese shares also fell. Investors are taking stock as they await additional market catalysts, said David Chao, global market strategist, Asia Pacific ex-Japan at Invesco. “We are also moving through peak tariff uncertainty, and these risks could be amplified in the coming weeks.”

In FX, the Bloomberg Dollar Spot Index rose 0.3% and above levels seen before Wednesday’s Federal Reserve decision after US equity futures abruptly turned lower. The pound slipped 0.3%, having risen earlier this week to the highest since November. The Bank of England is expected to leave its benchmark rate unchanged later, with fresh data showing that UK wage growth held at its highest level in nine months.

- EUR/USD drops as much as 0.6% to 1.0839, lowest in nearly a week

- GBP/USD down 0.3% to 1.2962; the Bank of England is likely to turn less dovish on Thursday as officials start to fret about the fallout from Donald Trump’s tariff wars and a renewed bout of domestic inflation

- EUR/CHF falls as much as 0.4% to 0.9531 before briefly reversing losses after the Swiss National Bank cut its interest rate to the lowest since September 2022 and declared another reduction is less likely for now

- EUR/SEK rallies by 0.4% to 11.0589, highest since March 14; Sweden’s central bank kept its benchmark rate unchanged at a two-year low and reiterated it’s finished with the easing cycle

- AUD/USD plummets by 1.1% to 0.6287; Australian employment surprisingly dropped in February, sending the currency and government bond yields lower as traders boosted bets on further interest-rate cuts this year

- USD/CAD up a third day, gains 0.4% to 1.4385; Canadian Prime Minister Mark Carney is poised to call a snap federal election on Sunday for an expected vote on April 28, the Globe and Mail reports

In rates, treasury futures push higher into early US session with yields falling across the curve. 10-year yields, lower by around 5bps at 4.19%, remain near richest levels of the session with bunds and gilts in the sector outperforming slightly, catching up with Wednesday’s post-FOMC moves in US rates. Investors continue to digest Wednesday’s Fed meeting, where Chair Powell said the inflationary impact of tariffs is likely to be transitory. US session features weekly jobless claims data at 8:30am New York time and a 10-year TIPS reopening at 1pm. Treasuries have added to their post-Fed gains, with US 10-year yields falling another ~3 bps to 4.21%. Gilts lead a rally in European government bonds ahead of the Bank of England decision, with UK 10-year borrowing costs falling nearly 6 bps to 4.57%. The pound falls 0.5%.

In commodities, Oil prices turn lower with Brent down 0.1% to $70.75 a barrel. Spot gold drops $19 to around $3,028/oz. Bitcoin inches lower toward $85,000.

Looking to the day ahead now, the main highlight will be all the central bank results. Today will also be heavy with data releases, including the March Philadelphia Fed business outlook, US existing home sales, UK January unemployment rate, Germany February PPI, and Eurozone January construction output. In terms of earnings releases, we can expect Nike, FedEx, Micron, Lennar, RWE, Accenture, and PDD Holdings.

Market Snapshot

- S&P 500 futures up 0.5% to 5,705.50

- STOXX Europe 600 up 0.2% to 556.27

- MXAP up 0.2% to 190.03

- MXAPJ little changed at 593.59

- Nikkei down 0.2% to 37,751.88

- Topix up 0.4% to 2,795.96

- Hang Seng Index down 2.2% to 24,219.95

- Shanghai Composite down 0.5% to 3,408.95

- Sensex up 1.2% to 76,379.80

- Australia S&P/ASX 200 up 1.2% to 7,918.89

- Kospi up 0.3% to 2,637.10

- German 10Y yield little changed at 2.78%

- Euro down 0.3% to $1.0874

- Brent Futures up 0.8% to $71.34/bbl

- Gold spot down 0.2% to $3,041.19

- US Dollar Index up 0.25% to 103.69

Top Overnight News

- US President Trump posts on Truth Social "The Fed would be MUCH better off CUTTING RATES as U.S.Tariffs start to transition (ease!) their way into the economy. Do the right thing. April 2nd is Liberation Day in America!!!"

- Canadian PM Carney is expected to call a snap election for April 28, according to Bloomberg citing Globe

- US imports of Canadian crude tumbled to 3.13 million barrels a day last week, the lowest since March 2023 as producers exhaust local stockpiles. BBG

- Trump is expected to sign an executive order on Thurs that seeks to eliminate the Dept. of Education, although it can’t be formally closed without an act of Congress. NYT

- Nvidia plans to spend several hundred billion dollars on US-made chips and electronics over the next four years, CEO Jensen Huang told the FT. Nvidia shares rose overnight and semiconductor peers also gained. BBG

- Trump’s tariffs are forcing Chinese exporters to look for alternative markets, potentially unleashing a new “China Shock” that will claim millions of jobs in emerging economies from Mexico to Indonesia. BBG

- US energy stocks are outperforming all other sectors in the S&P 500 despite weaker crude prices. They’ve been helped by lingering inflation anxiety, a supportive US administration and intensifying geopolitical tensions. BBG

- BofA total card spending +0.8% Y/Y (vs. 0.3% Feb avg.); biggest slowdowns were in entertainment and home improvement: BofA

- Chinese government bonds extended a recovery after the PBOC boosted short-term funding support. BBG

- The BOE may turn less dovish as officials start to fret about the fallout from tariffs and a renewed bout of domestic inflation. The MPC will probably leave the benchmark at 4.5% today and reiterate a cautious approach to further cuts. BBG

- The pace of British pay growth was little changed and there were others signs of stability in the jobs market, according to official data that contrasted with warnings of a hit to hiring from employers upset about an imminent tax increase. Private sector pay, excluding bonuses, - a key gauge for the Bank of England - rose by 6.1% in the three months to January, compared with the same period a year earlier, marginally slower than a 6.2% increase at the end of 2024, Thursday's data showed. RTRS

- Australia’s jobs numbers for Feb come in soft, with a ~53K drop in the number of employed people (the Street was looking for a 30K increase). WSJ

- Brazil’s central bank raised its benchmark rate by 100 bps to 14.25%, as expected. Policymakers signaled a smaller hike at their next meeting in May. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed with most indices in the green as the region initially took its cue from the gains on Wall St in the aftermath of the FOMC meeting where the Fed kept rates unchanged and slowed its balance sheet run-off, while Chinese markets bucked the trend and Japanese participants were absent due to Vernal Equinox Day. ASX 200 outperformed with gains led by the tech and real estate sectors amid a lower yield environment, while disappointing jobs data did little to derail the momentum in the index. KOSPI advanced amid strength in tech including index heavyweight Samsung Electronics which recently held its AGM and announced the appointment of one of its CEOs. Hang Seng and Shanghai Comp were subdued as participants navigated through earnings releases and after the lack of surprises from the announcement that China's benchmark Loan Prime Rates were kept unchanged.

Top Asian News

- HKMA maintained its base rate at 4.75%, as expected.

- US President Trump confirmed a willingness to hold a June summit with Chinese President Xi.

- Chinese battery makers CATL and BYD are targeted for new restrictions in the US under legislation that would bar the Homeland Security Department from procuring clean energy technology made by six companies, according to Nikkei Asia.

- South Korean opposition lawmakers are said to be seeking to impeach Acting President Choi, according to Yonhap citing the main DP opposition floor leader.

European bourses (STOXX 600 -1%) opened mixed, but has now succumbed to some significant selling pressure in recent trade, to display a negative picture in Europe. While there is no clear catalyst for the downside, it could be attributed to traders winding down their optimism surrounding the roll out of EU defence spending given it would take time to build up to spending of 1.5% of GDP; also, a pullback post-FOMC, refocussing on tariffs/trade into the April 2nd deadline and general economic/policy uncertainty all weigh. As such, a broad risk-off mood has entered markets since the European cash open, with the Dollar also catching a bid. European sectors are mixed and with the breadth of the market fairly narrow aside from the top/bottom performers. Retail takes the top spot, joined closely by Real Estate; the latter buoyed by the relatively lower yield environment – a factor which has led to some of the underperformance in Banks today.

Top European News

- ECB's Villeroy says "we cannot have a new policy of spending whatever it takes re. defence spending"; says could raise overall economic growth to 1.5% from 1% at present in the near future.

- ECB's Lagarde says ECB analysis suggests that a US tariff of 25% on imports from Europe would lower Euro Area growth by around 0.3ppts in the first year; reiterates data dependant approach. Says the analysis of bond yield shows increase in inflation expectations is not significant.

- SNB cuts its Policy Rate by 25bps to 0.25%, as expected; "prepared to intervene on the foreign exchange market as necessary". The SNB will continue to monitor the situation closely and adjust its monetary policy if necessary, to ensure that inflation remains within the range consistent with price stability over the medium term. SNB Vice Chair Tschudin says inflationary pressure should continue to ease gradually over the next quarters, particularly in Europe. Economic growth in Switzerland was solid in Q4, services sector and parts of manufacturing developed favourably, and there was a further slight increase in unemployment, while the utilisation of overall production capacity was normal. SNB's Schlegel says inflation has developed inline with expectations. Uncertainty about global economic developments and inflation has increased "significantly". Inflation is still being driven by domestic services. Will continue to monitor the situation closely and adjust our monetary policy if necessary. SNB Chair Schlegel (post-meeting Q&A) says monetary conditions are appropriate; will not comment on the value of the CHF.

- Riksbank Statement: Rates left unchanged at 2.25%; sees rates at current levels going forward.

- Norges Bank Regional Network Q1'25: "contacts report a pick-up in growth in 2025 Q1 and expect stable growth in Q2."

- Greek PM Mitsotakis supports the Commissions Defence White Paper; however, adds that at some point the EU will need to discuss whether they move to grants instead of loans to fund increased defence expenditure

FX

- DXY has continued to build on yesterday's post-FOMC gains with the release broadly as expected. The announcement failed to appease any of those in the market looking for a dovish lean from the FOMC with Chair Powell reaffirming that the Fed is in no hurry to cut rates. Ultimately, the Fed is in a holding pattern as policymakers look to gain clarity on the Trump administration's trade agenda. DXY has ventured as high as 103.95. If 104 gives way, interim resistance comes via the 14th March peak at 104.09.

- EUR is softer vs. the broadly firmer USD. From a macro perspective in the Eurozone, remarks from ECB President Lagarde largely echoed her introductory statement at this month's ECB press conference. However, she did flesh out the Bank's view on the ongoing trade conflict, noting that ECB analysis suggests that a US tariff of 25% on imports from Europe would lower Euro Area growth by around 0.3ppts in the first year. EUR/USD has slipped further from its YTD peak on Tuesday at 1.0954 and has hit a new low for the week at 1.0839.

- JPY flat vs. the USD and more resilient than peers. Yesterday, USD/JPY slumped beneath the 150.00 level as US yields softened in reaction to the Fed announcement, while the pair then continued its slide and approached closer to the 148.00 level in the absence of Japanese participants who were away from market overnight.

- GBP softer vs. the broadly firmer USD but stronger vs. the EUR. This morning's UK labour market report had no impact on expectations for today's upcoming BoE policy announcement. Cap Eco writes "the latest figures show that the jobs market is not collapsing as some surveys suggest and that there hasn’t been a big rise in the LFS redundancy rate". Cable is currently contained within yesterday's 1.2954-1.3010 range.

- Antipodeans are both at the bottom of the G10 leaderboard with pressure seen in AUD following disappointing jobs data from Australia which showed a surprise contraction in Employment Change and a drop in the Participation Rate, while better-than-expected New Zealand GDP failed to spur a bid.

- SNB delivered a 25bps cut to 0.25%, in-fitting with the majority of views and one that potentially takes the SNB to its terminal rate, with markets pricing in just 9bps of additional easing in 2025, though the still low inflation forecasts and uncertainty ahead (a point the SNB emphasised) mean further policy adjustments cannot be ruled out.

- PBoC set USD/CNY mid-point at 7.1754 vs exp. 7.2402 (Prev. 7.1697).

- Limited reaction seen in EUR/SEK following the widely-expected decision by the Riksbank to hold rates and the Riksbank declaring that it sees rates at current levels going forward, as reflected in the rate path. The lack of additional easing has been attributed to the recent higher-than-expected outturn for inflation.

- Brazil Central Bank hiked the Selic rate by 100bps to 14.25%, as expected, with the decision unanimous, while the committee expects another adjustment of a smaller magnitude at the next meeting and said the current scenario requires a more contractionary monetary policy.

- Morgan Stanley (MS) has paused its long EUR/USD and GBP/USD recommendations, saying investors may de-risk into the US' April 2nd tariff deadline. Adds that there is arguably too much EUR optimism priced in.

Fixed Income

- USTs are firmer as the benchmark continues the dovish move seen after the Fed with particular focus on the slowing of the balance sheet run-off. Action overnight was contained on account of no Japanese trade, but once cash trade resumed the benchmark continued its climb and is currently at a 111-06+ session high with yields lower across the curve which itself is flattening.

- Bunds are firmer, picked up most recently as the risk tone deteriorated in the European morning with specifics somewhat light but a lot of focus on global economic uncertainty into the April 2nd tariff date and digestion of the EU’s defence white paper. On this, WSJ’s Norman points out there are “reasons to be sceptical EU member states will spend EUR 650bln in additional defence spending” given new 1.5% of GDP flexibility in budget rules. Flexibility which implies that it will take time to reach such a spending level; a view which is potentially weighing on the risk tone.

- Gilts are outperforming on the back of reports that the Chancellor will announce the biggest spending cuts since austerity next week with cuts to Whitehall budgets by billions of pounds more than thought (the general view was already for significant cuts in the Spending Review). Additionally, the morning saw the latest employment data with wage metrics pretty much bang in line with expectations while the unemployment measures, via both LFS and Claimant Count, ticked higher. A point which was ultimately taken dovishly with markets now just about fully pricing a 25bps cut in June and another in November. Reporting/data which Gilts welcomed and, alongside continuing FOMC bullishness, saw the benchmark gap higher by 24 ticks before extending by 25 more to a 92.81 peak; the highest it has been since March 4th.

- Spain sells EUR 6.5bln vs exp. EUR 5.5-6.5bln 0.50% 2030 I/L, 3.15% 2035 & 3.45% 2043 Bono

Commodities

- Crude is a little lower, with initial overnight strength fading in the European session alongside the deterioration in risk tone and as the Dollar lifts to session highs. Brent'May currently in a USD 70.89-71.41/bbl range.

- Precious metals are pressured today, with spot gold lower by just under USD 4/oz, trading within a tight USD 3,038.78-3,057.51/oz range. The yellow-metal has cooled a touch from overnight highs, as the Dollar continues to strengthen.

- Base metals are mixed; 3M LME Copper extended on this week's rally overnight, and briefly reclaimed the USD 10k/t mark; though in-fitting with the risk tone, has cooled from those overnight peaks to a currently USD 9,930/t.

- US President Trump considers extending Chevron's licence to pump oil in Venezuela, according to WSJ.

- US Energy Secretary Wright confirmed the signing of the LNG export approval for the CP2 project on Wednesday and said they are moving urgently to grow supply of electricity and lower prices with the impact of administration moves expected to be seen later this year, while he also stated they want to grow supply and push oil prices down.

- Norway (Prelim) Feb oil production 1.72mln/bpd (prev. M/M 1.78mln/bpd); Gas Production 9.9bln (prev. 10.7bln) Cubic Metres

Geopolitics: Middle East

- Iran Foreign Minister says US President Trump letter is 'more of a threat', but adds that there are opportunities, and Tehran will contemplate both.

- Israeli military announced sirens sounded in several areas in Israel following a projectile that was launched from Yemen, while Houthis said they shelled Ben Gurion Airport with missiles and bombarded US aircraft carrier Harry Truman with a number of ballistic and winged missiles and drones, according to Asharq News.

- Houthi media reported the US bombing of targets including a cotton factory in Zabid district and with five raids in Hodeidah, northwestern Yemen, according to Sky News Arabia

- US President Trump's letter to Iran's Supreme Leader Ali Khamenei included a two-month deadline for reaching a new nuclear deal, according to Axios citing sources.

- US Secretary of State Rubio says President Trump seeks to promote peace and resolve the issue of "Iranian nuclear" diplomatically but is ready for all options, while he added that if Trump is forced to choose between a nuclear Iran or take action to prevent that from happening, he will take action.

- French President Macron said he spoke with Saudi Arabia’s Crown Prince MBS and welcomed the Jeddah Initiative, which enabled the start of peace negotiations in Ukraine, while Macron condemned the resumption of Israeli strikes on Gaza and said the conference on a two-state solution, which France will co-chair, must help revive a political perspective for both Israelis and Palestinians.

Geopolitics: Ukraine

- Russian Kremlin says, on a US-Russia meeting in Jeddah, that it may not be on Sunday but will be in the coming days. Will announce who the Russian representative will be. To discuss the Black Sea initiative and other points of the Ukrainian peace deal.

- Ukrainian President Zelensky said Ukrainian and US officials may meet this Friday, Saturday or Sunday, while he added that his conversation with Trump on Wednesday was substantive and he felt no pressure from Trump. Zelensky said Ukraine is ready to discuss US involvement in the Zaporizhzhia plant's restoration with discussions in the early stages and noted it is not yet clear exactly how the infrastructure ceasefire will be monitored. Furthermore, he said Ukraine will respond in kind if Russia violates the ceasefire and that President Trump understands that Ukraine will not recognise occupied land as Russian.

US Event Calendar

- 08:30: March Initial Jobless Claims, est. 224,000, prior 220,000

- 08:30: March Continuing Claims, est. 1.89m, prior 1.87m

- 08:30: 4Q Current Account Balance, est. -$330b, prior -$310.9b

- 08:30: March Philadelphia Fed Business Outl, est. 9.0, prior 18.1

- 10:00: Feb. Existing Home Sales MoM, est. -3.2%, prior -4.9%

DB's Jim Reid concludes the overnight wrap

Although yesterday was a day where the market rallied on a relatively dovish Fed meeting, at least in terms of Powell's messaging, the most interesting thing I listened to over the course of the day was a podcast featuring US Treasury Secretary Bessent. I’ll be honest that my walk to the station in the morning is usually accompanied by a tub-thumping Liverpool podcast. However since they were dumped out of Europe and lost a cup final in the course of the last week, I’m avoiding them for now. So as there were no new golf podcasts available, I listened to Bessent. I suppose the more you listen to this administration the more the evidence builds that they are serious about making significant structural changes to the economy. Here he talked about reducing the role of government, the fact that after WWII 90% of Americans made more than their parents and now it's 50/50, and the distributional problems of the top 10% owning large amounts of assets with the bottom 50% not having much. Anyway it's worth a listen. It's within the All-In podcast.

Bessent did say he completely respected the Fed's autonomy on monetary policy even if he didn’t always agree with them. There wasn’t a lot of incremental news to agree or disagree with last night as they kept the fed funds rate on hold in the 4.25%-4.50% range for a second consecutive meeting, while announcing a slowing in the pace of QT. The updated dot plot showed the median FOMC member still expecting two rate cuts in 2025, even as the distribution of responses shifted in a more hawkish direction with 8 of the 19 members expecting one or no cuts this year. The projections also saw 2025 core inflation revised +0.3pp higher and growth -0.4pp lower, with the balance of risks also shifting in a more stagflationary direction. A clear majority of the FOMC now see risks tilted towards higher inflation but towards weaker growth and higher unemployment.

In the press conference, Powell reiterated that policy was in a “good place” and that the Fed is not in a “hurry” to cut rates, while emphasising the “remarkably high” uncertainty and avoiding potential hawkish signals. He acknowledged that tariffs may delay “further progress” on inflation but said that the base case was the tariff impact on inflation would be “transitory” and noted that long-term inflation expectations remained anchored. Powell said the Fed was watchful of risks from the recent downturn in sentiment data though the relationship with hard data had not been “very tight” lately. Our US economists think that while the Fed may be anticipating a slowdown in the hard data, they are on hold until that evidence emerges (see their reaction here).

On the balance sheet, the Fed announced a slowing in the pace of QT, with the runoff in Treasury holdings to slow from $25bn to $5bn from April 1, while the MBS redemption cap was unchanged at $35bn. The move matched our expectations that an adjustment of QT was likely, though the details were somewhat different with Powell saying that the FOMC had “seen some signs of increased tightness in money markets” and reusing a “slower for longer” argument adopted when the Fed first slowed QT last May. See our rates strategists' takeaway here.

Rates saw a solid rally on the back of the decisions, with 10yr yield having traded 3-4bps higher on the day prior to Fed before closing -4.1bps lower at 4.24%. 2yr yields saw a larger move, falling by -11bps post-FOMC to close -6.8bps lower on the day. The amount of Fed rate cuts priced by year-end rose +6.7bps to 66bps from its three-week low the previous day. The avoidance of a hawkish Fed surprise also boosted equities, with the S&P 500 rallying from +0.3% pre-FOMC to as much as +1.8% higher near the end of Powell’s press conference, before closing up +1.08%. The rally was broad-based with all 11 major S&P sector groups higher on the day. The Mag-7 (+1.67%) reversed much of the previous day’s -2.47% loss, while the VIX closed below the 20 level for first time since the end of February (-1.90pts to 19.90).

Ahead of the Fed’s decision, European equity markets had mostly seen modest gains, with the STOXX 600 rising +0.19%, led by gains for the CAC (+0.70%) and FTSE MIB (+0.45%). The DAX (-0.40%) underperformed for once, largely due to losses in its auto and defence stocks including notable declines for Rheinmetall (-4.53%) and Saab (-5.33%). European bonds saw a modest rally, with 10yr bund yields -0.8bps lower at 2.80%.

Those moves came as EU leaders presented their white paper on “Readiness 2030”, with European Commission President Ursula von der Leyen saying “we must buy more European” and create an “EU-wide” market for defence equipment. With much of the detail having already been well flagged in recent weeks, there was a hint of disappointment on the announcement. Notably, the EU announced that the US, UK and Turkiye will be excluded from the €150bn EU defence spending fund unless they sign defence and security pacts with the EU. The UK’s exclusion in particular was a surprise since PM Keir Starmer has been very vocal about the UK’s commitment to increased defence funding and cooperation on European defence. The UK is attempting to balance on a geopolitical tightrope between trying to get closer to the EU again after years of Brexit, but also trying to avoid the worst impact of Trump’s April 2 tariff deadline. The FT reported yesterday that the UK is engaging with Trump’s trade team over things like dropping the UK’s digital services tax in return for reduced tariffs.

Earlier yesterday morning, the European mood had seen some contagion from the news that Turkish authorities had detained Istanbul Mayor Ekrem Imamoglu, who is seen as a top political rival to Turkiye’s President Erdogan. The Turkish Lira saw an initial steep decline of as much as -11.15%, though it recovered to-3.19% by the close. Other Turkish assets also struggled, with the ISE equity index down -8.72% on the day and yields on Turkish 10Y dollar bonds rising +15.5bps to +7.38%. The news contributed to the euro (-0.38%) posting its worst day against the dollar so far this month after reaching a 5-month high on Tuesday.

Elsewhere in Europe yesterday, TTF natural gas futures (+8.46%) saw their biggest jump in nearly three weeks after the limited progress from the Trump-Putin call on Tuesday evening. Ukraine’s President Zelensky agreed to halt strikes on energy assets following a call with Trump yesterday, echoing a similar agreement between Trump and Putin the previous evening, but questions over the exact details of this remained.

Looking forward to today, Europe will see a triple header of central bank policy decisions from the SNB, Riksbank and BoE. On the SNB we are expecting a 25bp cut, in line with consensus. On the Riksbank, we think things are skewed towards a hold with hawkish messaging. Lastly on the BOE, the expectation is for a hold at 4.5% and a relatively quiet meeting (see our UK economist’s preview here).

Asian equity markets are showing a mixed performance this morning. Across the region, the Hang Seng (-1.18%) is leading losses, falling from a three-year high amid a pullback in technology stocks from their recent rally. The CSI (-0.39%) and the Shanghai Composite (-0.10%) are also edging lower. By contrast, the S&P/ASX 200 (+1.18%) is continuing to recover from a recent seven-month low as risk sentiment was boosted by softer-than-expected employment data (more below). The KOSPI (+0.33%) is also trading in positive territory. Elsewhere, Japanese markets are shut for a holiday. Outside of Asia, US stock futures are indicating a positive start, with those on the S&P 500 (+0.48%) and NASDAQ 100 (+0.66%) moving higher. Cash Treasuries are shut in Asia due to the holiday in Japan.

Coming back to Australia, the employment rate dropped sharply by -52.8k in February (v/s +30.5k in January), significantly missing market expectations of +30k gain. The broad-based decline raised expectations for an interest rate cut by the RBA.

On the monetary front, the People’s Bank of China (PBOC) kept the 1-year loan prime rate (LPR) at 3.1% and the 5-year LPR at 3.6%, where they have been since a quarter-percentage-point cut in October.

To the day ahead now, the main highlight will be all the central bank results. Today will also be heavy with data releases, including the March Philadelphia Fed business outlook, US existing home sales, UK January unemployment rate, Germany February PPI, and Eurozone January construction output. In terms of earnings releases, we can expect Nike, FedEx, Micron, Lennar, RWE, Accenture, and PDD Holdings.